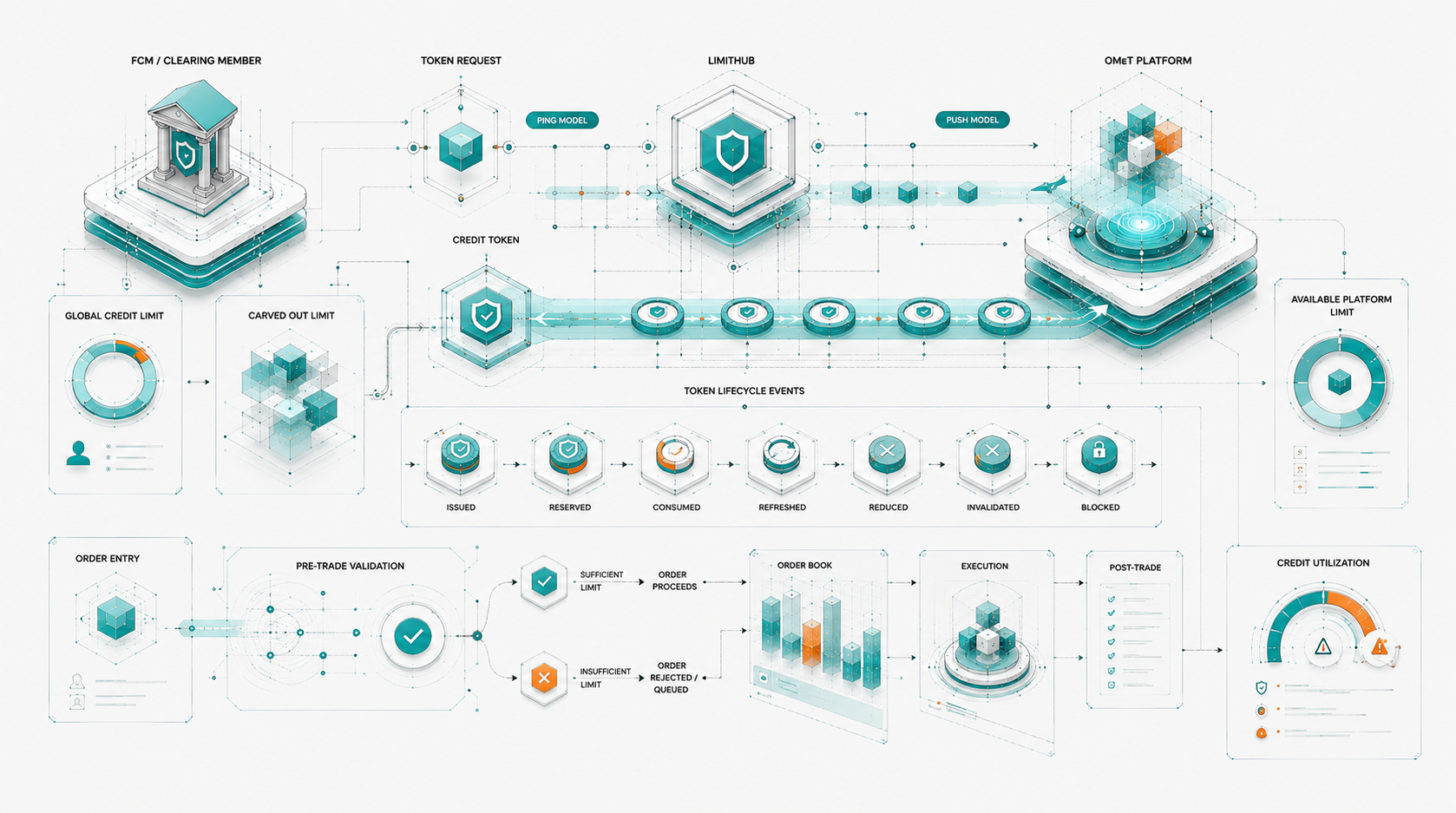

Account hierarchy is the foundation. A participant may operate through house accounts, client accounts, sub-accounts, trading desks, portfolio sleeves, or strategy-level books, and each structure must be represented clearly before trading begins. Internal OMeT discussions note that limits may need to govern “various House accounts” for self-clearing users and that those limits should be addressed directly during onboarding. This hierarchy determines who can trade, where the trade is booked, which limits apply, and how the transaction flows into clearing and reporting.

Clearing firm linking is the second critical layer. OMeT supports multiple clearing venues, including CME, LCH, and Asigna, but those venues are not interchangeable at the user level. Internal discussions state that clients are onboarded with clearing accounts at the respective clearinghouse where they want to direct trades, and that CME, LCH, and Asigna are not fungible clearing destinations. For external clients using an FCM, the FCM may set the relevant limit; for self-clearing members, the onboarding process must define the platform limits that govern their own accounts.

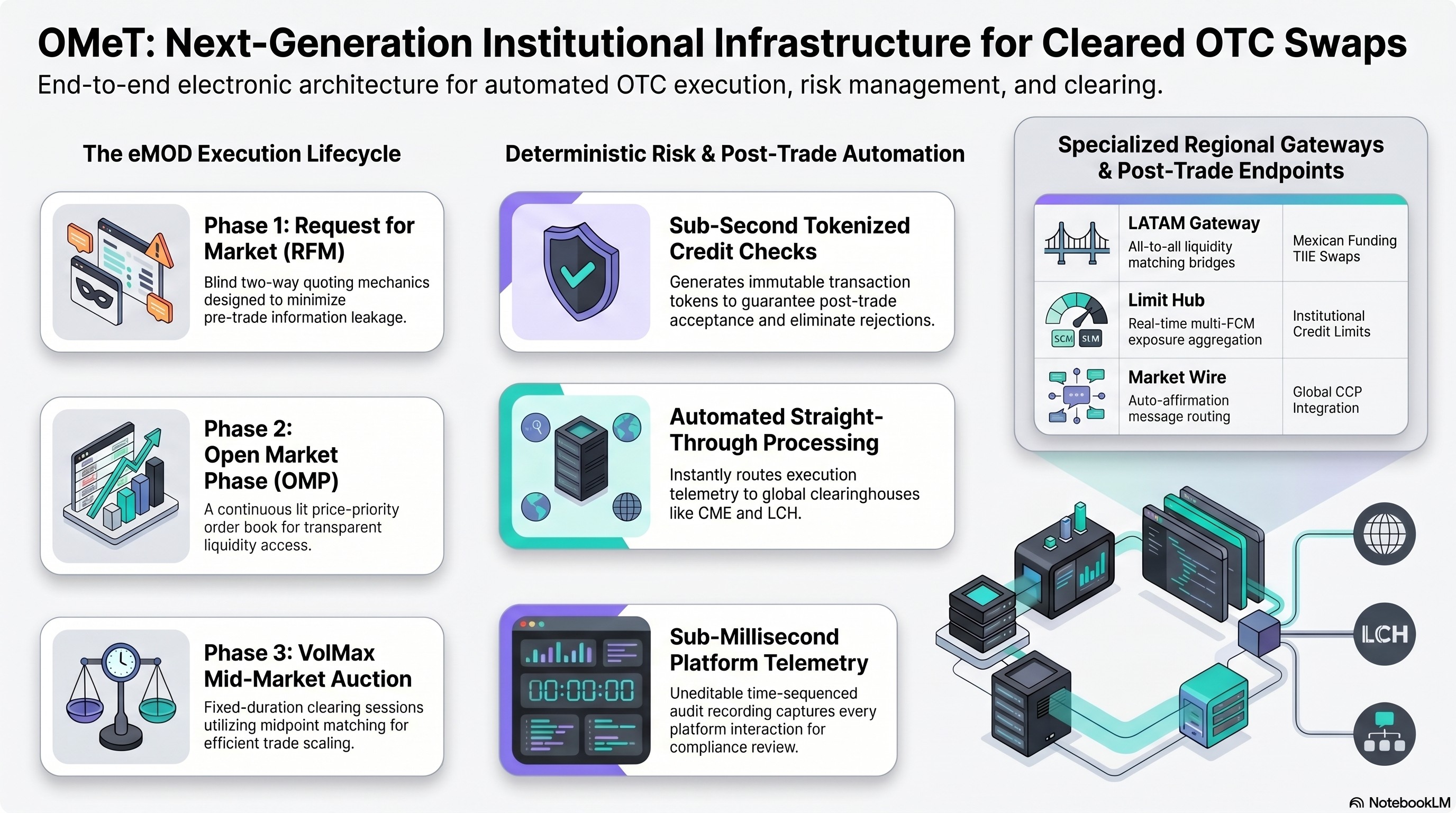

Profile deployment brings these components together into a live trading configuration. The participant profile should encode firm identity, desk permissions, instrument access, clearing eligibility, FCM or self-clearing linkage, account hierarchy, limit source, and post-trade routing instructions. OMeT’s external connectivity model reinforces why this setup matters: Market Wire plays a foundational role in post-trade processing and clearinghouse connectivity, helping support anonymity, pre-trade certainty, and sub-second execution-to-processing workflow. In practical terms, onboarding is not administrative setup; it is the control plane that determines whether a participant can safely move from login to execution to cleared acceptance.