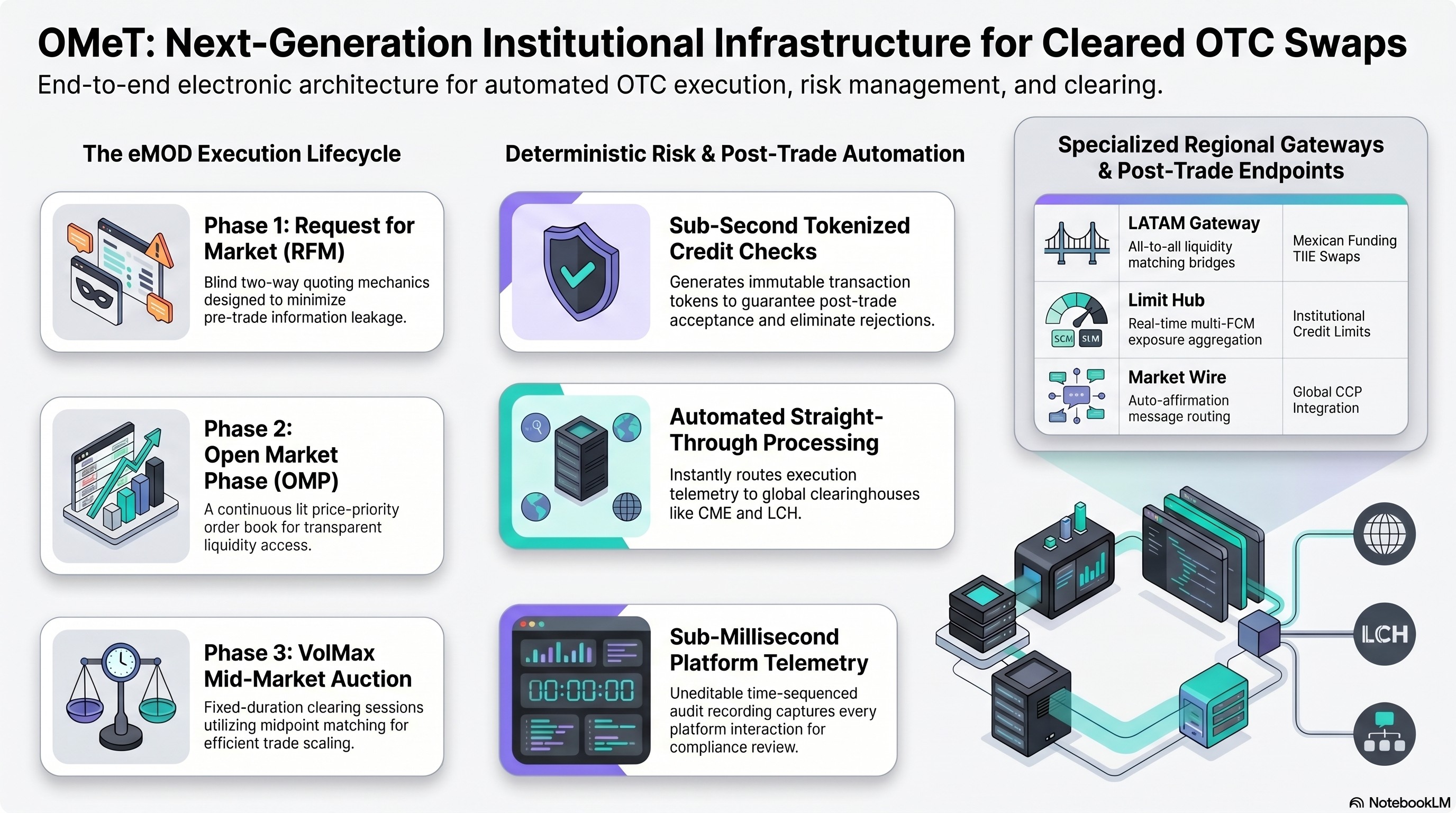

Liquidity Providers on OMeT operate inside a rules-based execution workflow rather than a discretionary voice-broker model. Their role is to supply responsive pricing during the relevant phase of the eMOD lifecycle, especially when a Request for Market is launched and eligible LPs are asked to show executable interest. Internal product discussions describe participants being able to respond to an RFM or enter orders that may interact with the broader session structure, reinforcing that LP activity is governed by the phase state rather than informal bilateral negotiation.

Responsive quoting is most important in the RFM phase, where the requester seeks pricing without immediately exposing the full trade into a lit market. LPs are expected to provide structured market responses that can move the session toward execution or, if not fully completed, into the next phase. OMeT’s design gives banks and market makers a meaningful opportunity to provide liquidity early, and internal discussions emphasize preserving market-maker participation because the platform’s goal is to attract real liquidity rather than merely display one-sided interest.

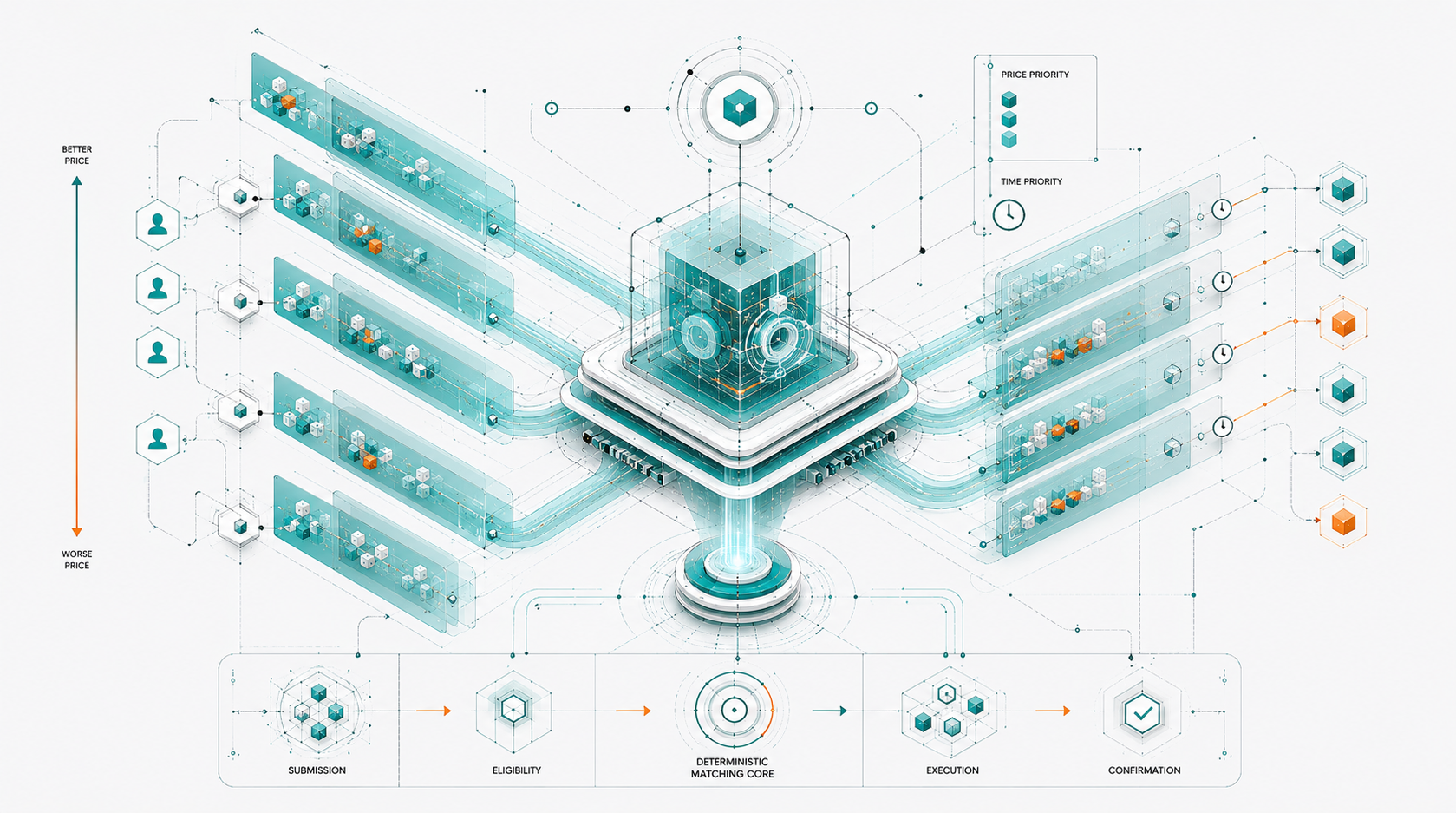

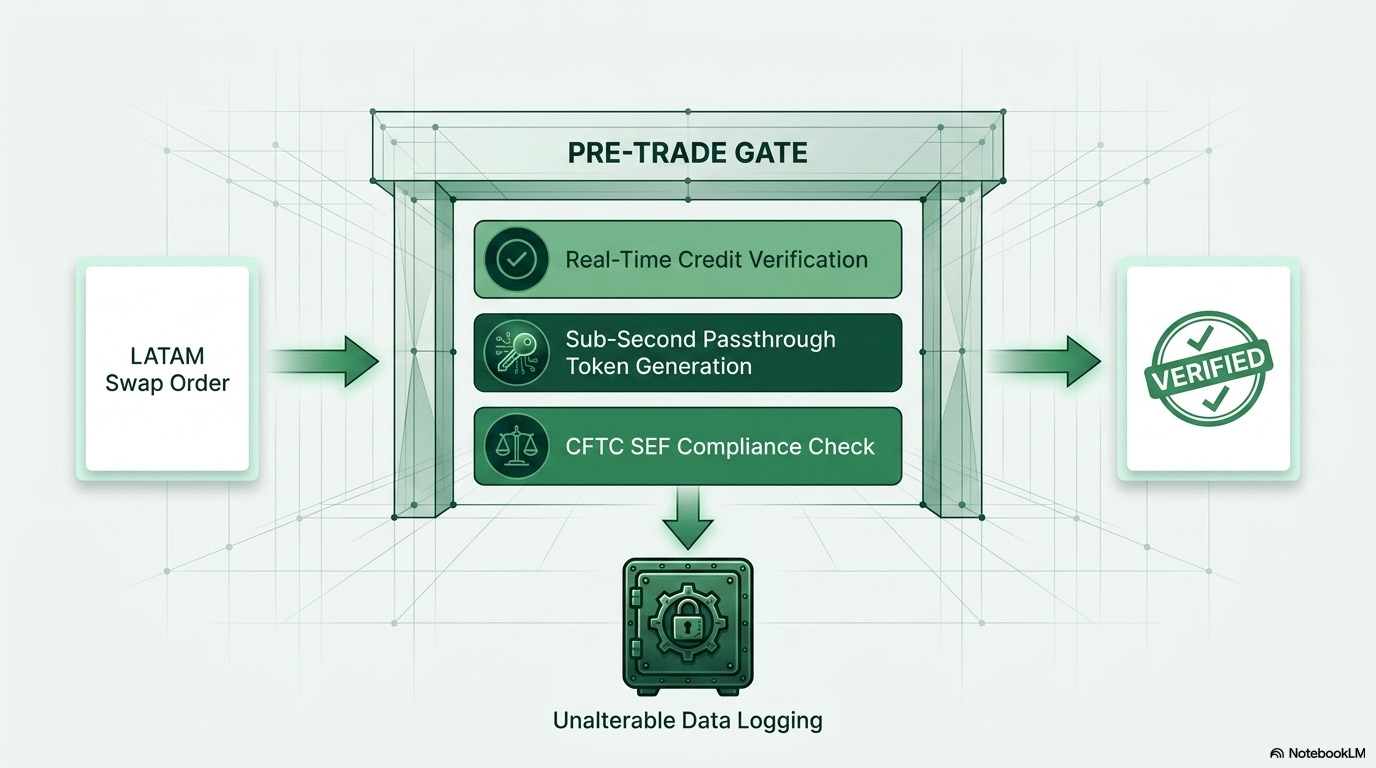

Spread constraints define the quality control around LP participation. In the Open Market Phase, OMeT materials describe a lit market where bids and offers are visible to all participants, with a default maximum bid-offer spread of one basis point. If the RFM requester asks for a tighter spread, OMP reverts to the one-basis-point default; if the requester asks for a wider spread, that wider restriction can carry into OMP to avoid invalid market behavior. Crosses are not allowed in OMP, and orders through the prevailing market may be rejected or executed at the existing market level.

LP obligations change as the session progresses. In RFM, the LP’s role is to provide responsive, controlled pricing. In OMP, the LP competes in a transparent order-book environment where displayed bids and offers help form the market. When the market becomes stale and transitions to VolMax, spread control no longer applies in the same way because the phase becomes a midpoint matching mechanism based on the last valid OMP bid and offer, with fills allocated by time priority at the mid-price. This multi-phase structure gives LPs clear operating rules: quote responsively, respect spread and market-state constraints, and participate within deterministic session logic from private request through lit competition and residual midpoint matching.