What is information leakage?

Information leakage occurs when a trader’s intent becomes visible to the market before the trade is complete.

In OTC derivatives, the leaked information may include:

- Who is looking to trade

- What direction they want to trade

- How large the order may be

- How urgent the execution is

- Which dealers have been contacted

- Whether the trader is testing price or committed to execute

- Whether the trade is likely to clear

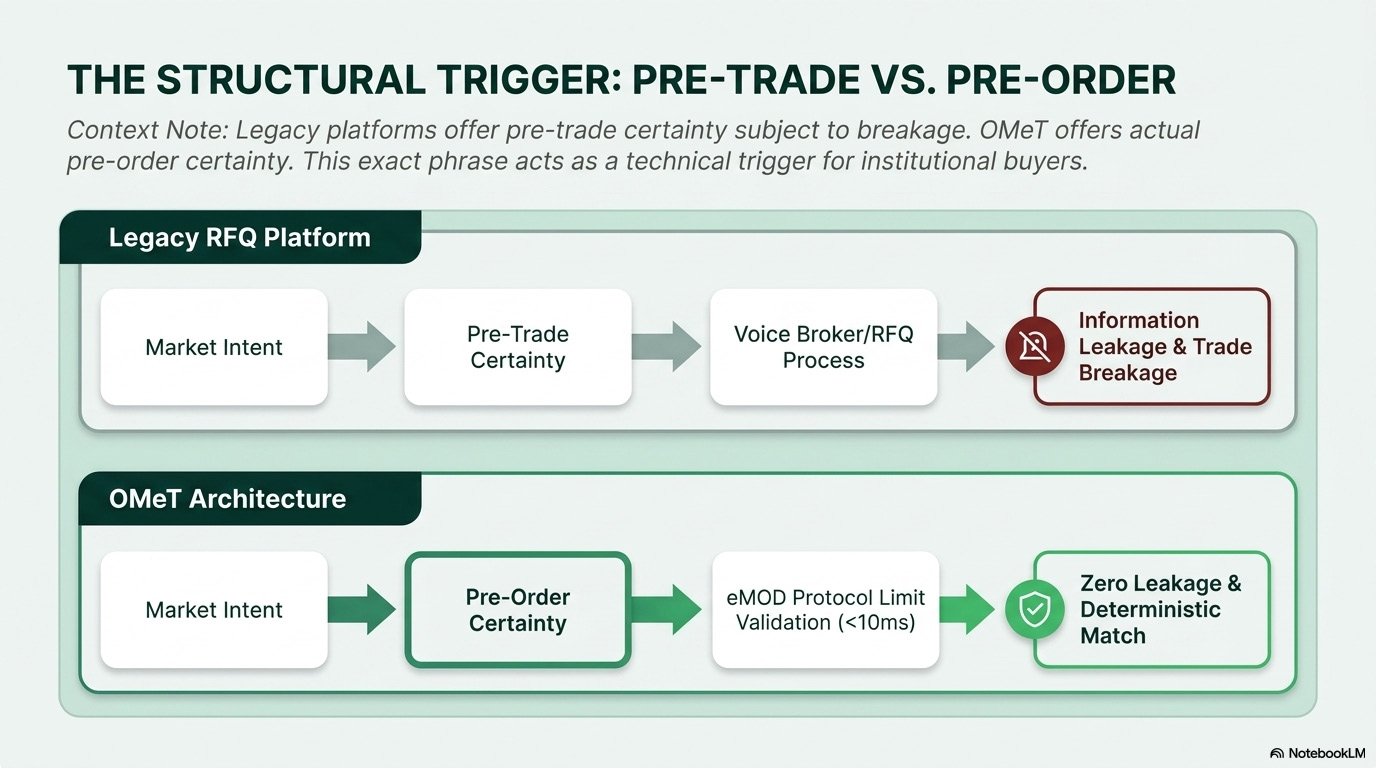

Legacy execution workflows often require traders to expose these details as part of the process of finding liquidity. This is especially true in voice-brokered markets and RFQ models, where the search for price can become a signal in itself.

The result is a quiet execution tax. The trader may not see a direct fee line item, but the cost can appear through wider markets, reduced dealer willingness, adverse price movement, or diminished block-trade efficiency.

Why legacy voice and RFQ workflows create exposure

Voice brokerage and RFQ workflows were built around relationship-based liquidity discovery. That structure can be useful in certain markets, but it creates a difficult trade-off for institutional traders.

To find liquidity, the trader often has to reveal intent.

In a voice process, the broker may need to know the client, the direction, the approximate size, and the urgency in order to search for the other side. In an RFQ process, the trader may expose a request to multiple dealers at once. Even when identities are partially controlled, the pattern of inquiry may still provide enough context for the market to infer what is happening.

This creates three practical vulnerabilities.

1. Identity exposure

When the market knows who is trading, it may infer motive. A large asset manager, hedge fund, bank desk, or regional institution may each carry different signaling value. Identity can influence pricing behavior before the actual order is matched.

2. Directional exposure

A request to pay, receive, buy, sell, hedge, unwind, or restructure can move the market before execution. In illiquid instruments, even a small number of informed participants may be enough to change the available price.

3. Size exposure

Block trades create special leakage risk. The larger the order, the more valuable the information becomes. Once the market understands that a large buyer or seller exists, liquidity providers may adjust pricing, reduce displayed interest, or wait for better economics.

Why this matters most in illiquid OTC swaps

Information leakage is most damaging when liquidity is scarce.

In highly liquid markets, the impact of a single inquiry may be absorbed by market depth. In illiquid OTC swaps, however, liquidity may depend on a small group of participants, specific clearing constraints, local market expertise, and dealer balance-sheet appetite.

That means the execution path itself becomes part of the price formation process.

A trader may believe they are searching for liquidity, but the act of searching can alter the liquidity available. The more fragmented the process, the greater the risk that pre-trade communication becomes market information.

This is why reducing slippage in OTC swaps requires more than better pricing screens. It requires a different execution architecture.

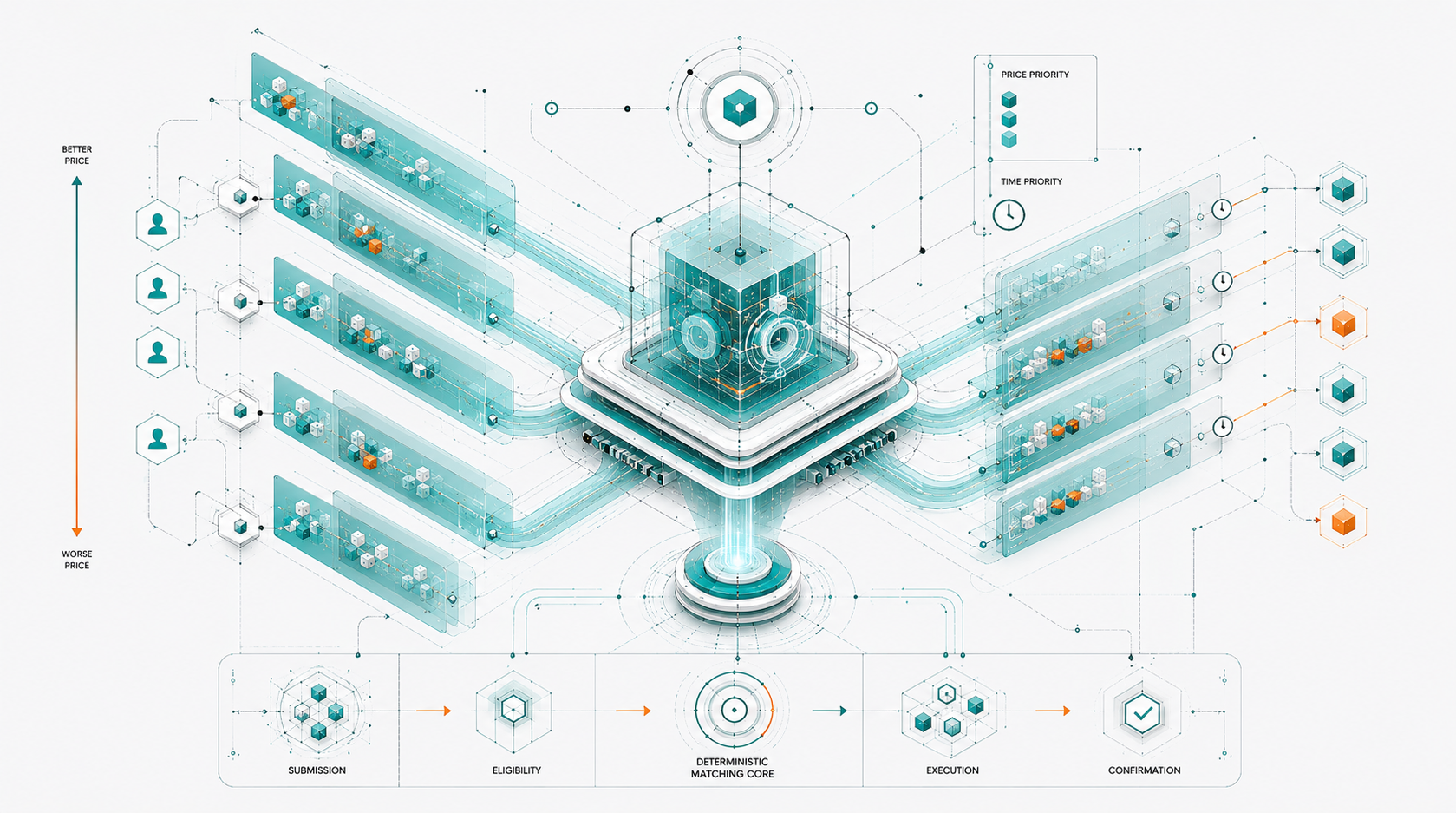

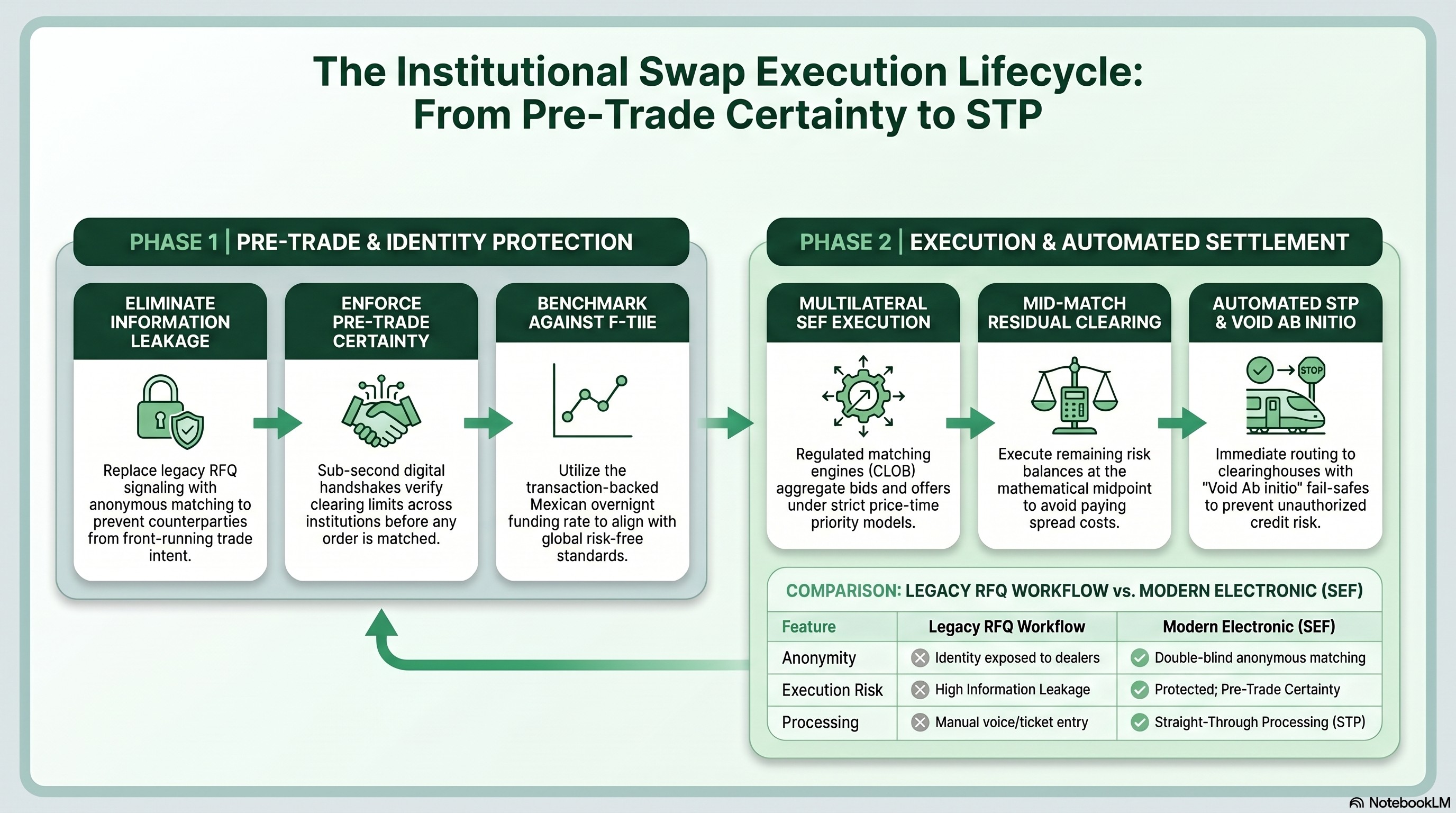

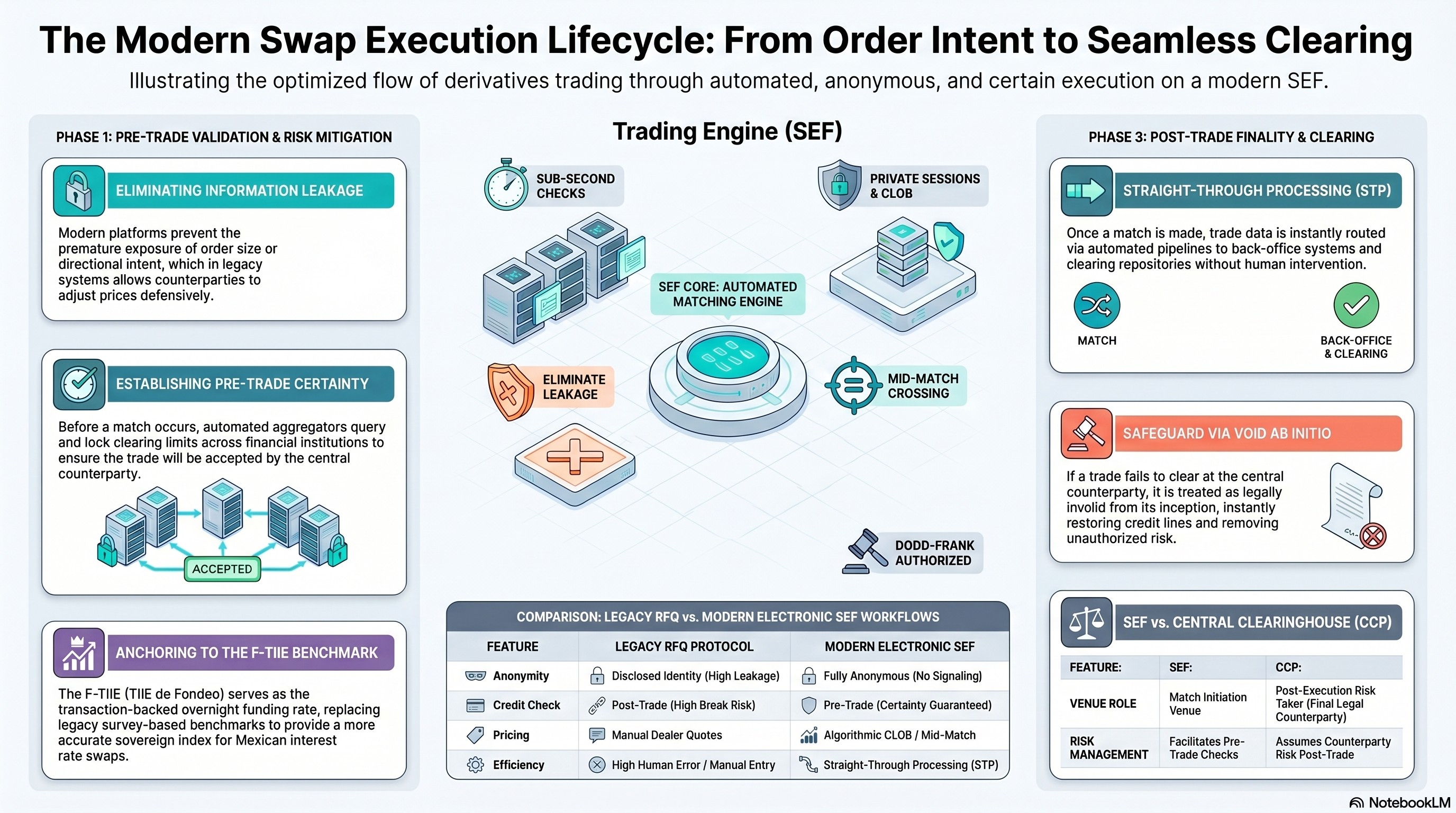

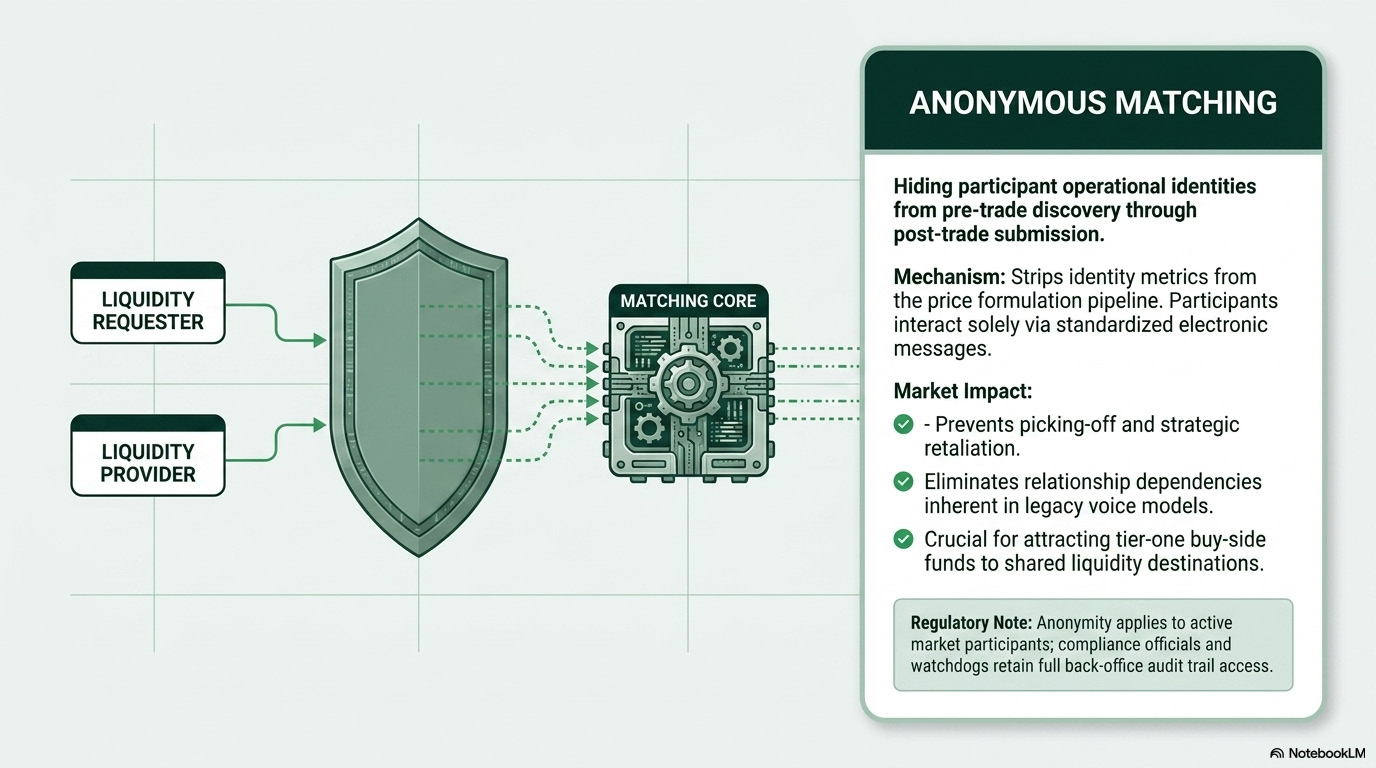

How an anonymous, rules-based matching engine helps

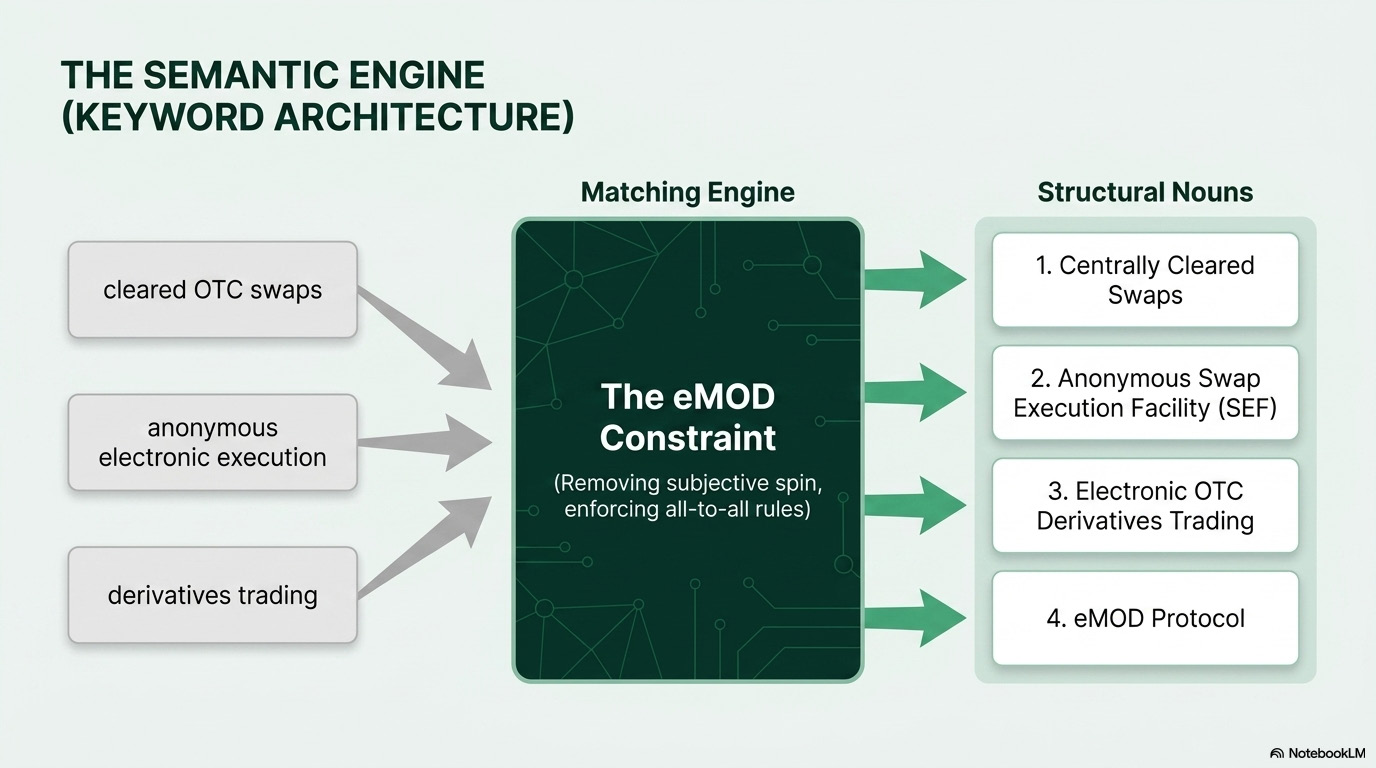

An anonymous, rules-based matching engine is designed to reduce unnecessary signaling before execution.

Instead of asking traders to reveal intent through sequential conversations or broad RFQs, the venue can structure the process around defined execution rules. Participants interact with the market through controlled order logic rather than exposed bilateral negotiation.

The goal is not to eliminate all market risk. It is to reduce avoidable information risk.

A properly designed matching engine can support:

- Anonymous interaction before execution

- Standardized order-entry conditions

- Pre-defined matching rules

- Reduced discretionary signaling

- Consistent treatment of eligible participants

- Clear execution records

- Integration with clearing and post-trade workflows

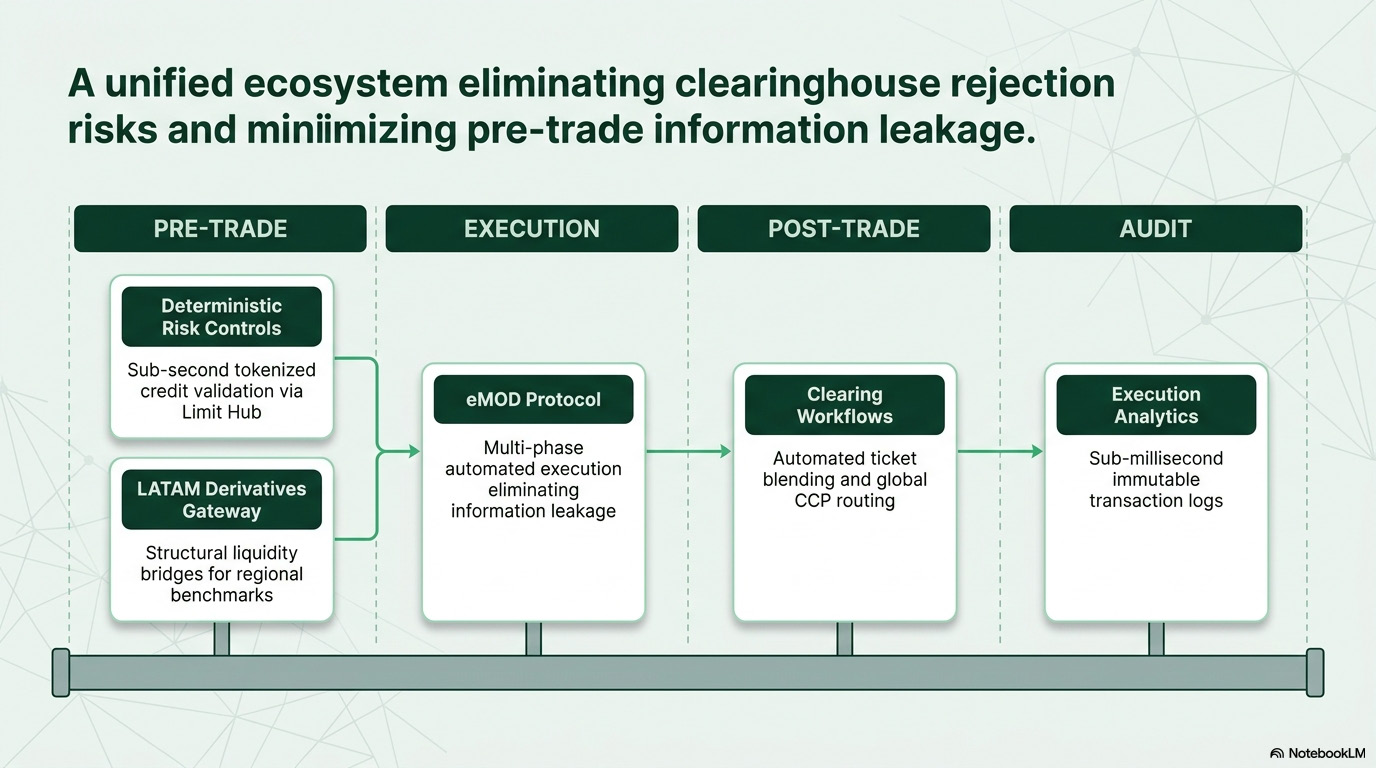

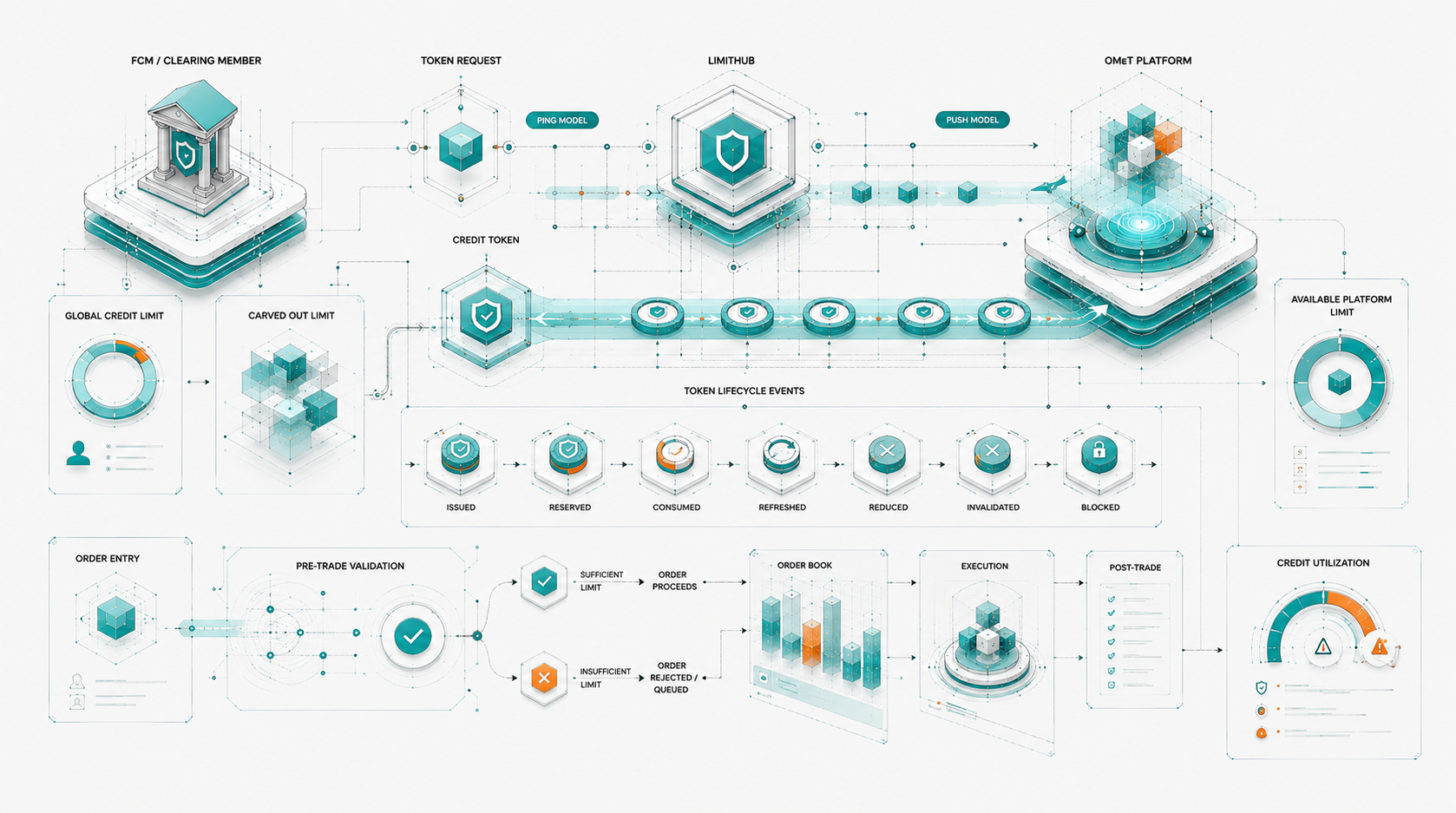

OMeT’s internal site strategy describes the platform as a deterministic execution ecosystem for cleared OTC markets, designed to support execution, allocation, post-trade workflow, and market intelligence in one environment. That positioning is directly relevant to slippage and leakage because the issue is not just price discovery. It is the structure of the workflow that creates or contains the signal.

How it works in OMeT

In an OMeT-style execution model, the trader’s objective is translated into a controlled, rules-based workflow.

Rather than exposing full intent through a series of manual conversations, the trader enters execution interest into a system designed to manage how and when information is revealed. Matching logic determines whether compatible interest exists. Where credit, clearing, allocation, or post-trade processing constraints are relevant, those constraints can be incorporated into the broader workflow rather than handled manually after the fact.

This matters because many legacy workflows separate the execution event from the operational consequences of the trade. A trader may discover price first and validate clearing or post-trade details later. That creates another source of risk: the trade may appear executable before the workflow is actually ready to support it.

OMeT’s broader solutions positioning ties execution to allocation, processing, and market intelligence rather than treating execution as a standalone click event. That integrated structure is important for institutional buyers because leakage often happens across workflow handoffs, not only at the moment of price formation.

A practical blueprint for reducing leakage

Institutions seeking to reduce slippage and information leakage should evaluate their execution workflow across five control points.

1. Control what is revealed before execution

The first question is simple: what does the market learn before the trade is done?

A leakage-resistant workflow should minimize unnecessary disclosure of identity, direction, size, and urgency. Traders should not have to broadcast intent merely to discover whether executable interest exists.

2. Separate liquidity discovery from identity disclosure

In legacy markets, the search for liquidity is often tied to relationship disclosure. An anonymous matching model changes that sequence. Liquidity can be tested through rules and eligibility rather than through exposed bilateral conversation.

3. Standardize execution conditions

Manual negotiation introduces discretion. Discretion can create inconsistency, delay, and signaling risk. Rules-based execution conditions help participants understand how matching occurs and reduce the need for interpretive back-and-forth.

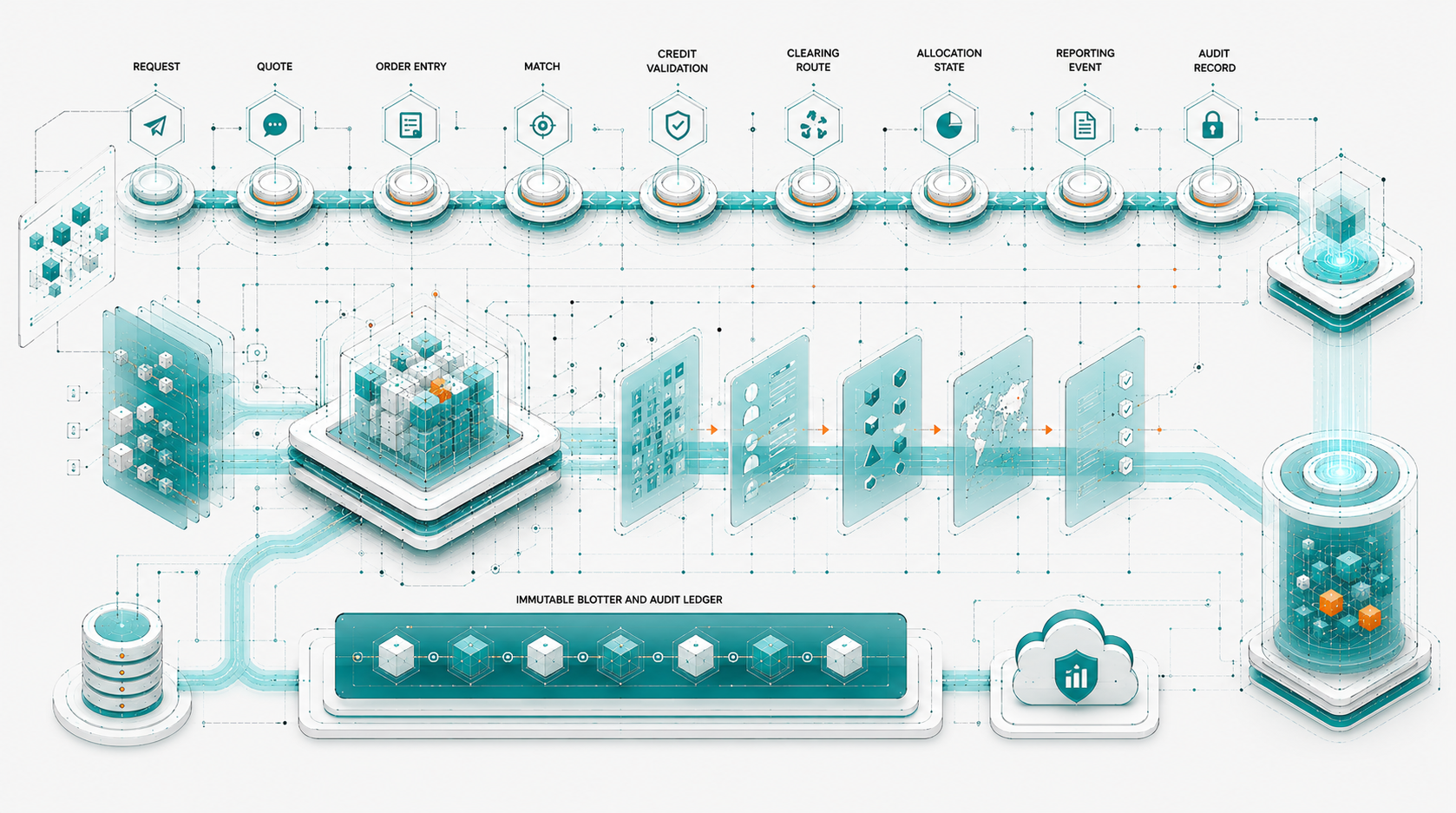

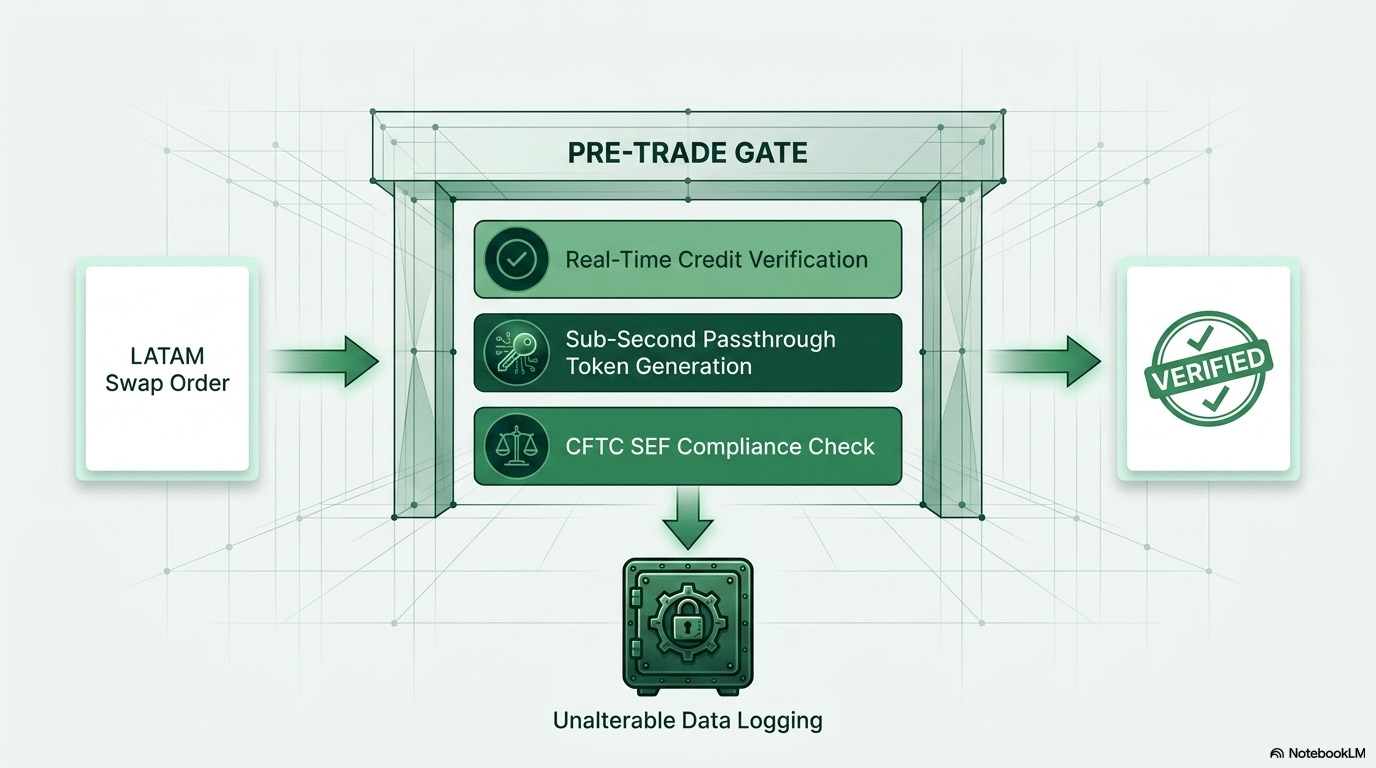

4. Integrate pre-trade controls

A trade that cannot clear is not a clean execution. Pre-trade controls help reduce the risk that a matched order later fails because of credit, clearing, or operational constraints. This is especially important in cleared OTC markets where execution quality cannot be separated from clearing certainty.

5. Preserve audit-ready records

A strong workflow should create a clear record of what happened, when it happened, and under which rules. That record supports compliance, supervision, post-trade review, and future execution analysis.

Who is this for?

This subject is most relevant for institutional teams that trade or supervise illiquid cleared OTC derivatives.

Heads of trading

For heads of trading, the priority is execution quality. Reducing leakage can improve the trader’s ability to access liquidity without unnecessarily moving the market.

Portfolio managers

For portfolio managers, the issue is implementation drag. A strategy may be correct, but excessive leakage can reduce realized performance during execution.

Risk officers

For risk officers, the issue is workflow control. A rules-based model can reduce the uncertainty created by manual negotiation, post-trade breaks, or unclear execution conditions.

Compliance officers

For compliance teams, the issue is supervision. A deterministic workflow with clear execution records is easier to review than fragmented conversations across voice, chat, email, and dealer platforms.

Operations leaders

For operations teams, the issue is downstream efficiency. When execution, allocation, clearing, and processing are connected, there is less room for manual repair after the trade.

Benefits

A more controlled execution architecture can produce several institutional benefits.

Reduced pre-trade signaling

The market receives less information before the trade is ready to execute.

Cleaner block-trade handling

Large trades can be managed with greater attention to anonymity, size control, and execution sequencing.

More consistent execution logic

Rules-based matching reduces dependence on informal process, broker discretion, or inconsistent bilateral negotiation.

Better alignment with clearing workflows

Execution can be designed with clearing and post-trade requirements in mind rather than treated as a separate event.

Stronger institutional oversight

Audit-ready records help compliance, risk, and trading supervision teams understand how execution occurred.

Limitations

Anonymous, rules-based execution does not remove every execution cost.

Markets can still move. Liquidity can still be limited. Participants may still price conservatively in volatile conditions. A matching engine cannot manufacture natural liquidity where none exists.

The more precise claim is that controlled execution infrastructure can reduce avoidable leakage created by the workflow itself.

That distinction matters. The objective is not to promise perfect execution. The objective is to remove unnecessary structural friction from the execution process.

This aligns with OMeT’s broader communication posture: restrained, factual, and focused on deterministic mechanics rather than exaggerated claims. Internal OMeT messaging guidance specifically emphasizes institutional language and avoids hype-driven “disruptor” framing.

Why the old workflow is becoming harder to defend

For many years, voice and RFQ workflows persisted because they reflected how OTC markets actually operated: relationship-driven, fragmented, and dependent on human intermediation.

But institutional expectations have changed.

Trading teams now need more than access. They need control. Risk teams need pre-trade certainty. Compliance teams need records. Operations teams need straight-through processing. Technology teams need infrastructure that can be integrated, monitored, and improved.

The problem is not that every legacy workflow is broken. The problem is that legacy workflows often force institutions to solve modern execution problems with tools designed for a less automated market structure.

Slippage and information leakage are symptoms of that mismatch.

Conclusion

Reducing slippage in illiquid OTC swaps begins with reducing unnecessary information leakage.

Voice and RFQ workflows often require traders to reveal intent as the cost of finding liquidity. In block trades and less liquid instruments, that disclosure can become expensive before the trade is even executed.

A more durable model uses anonymity, rules-based matching, pre-trade controls, and integrated post-trade workflow to limit avoidable signaling. For institutional traders, the core question is no longer only “Where is the best price?” It is also: “How much did we reveal to find it?”