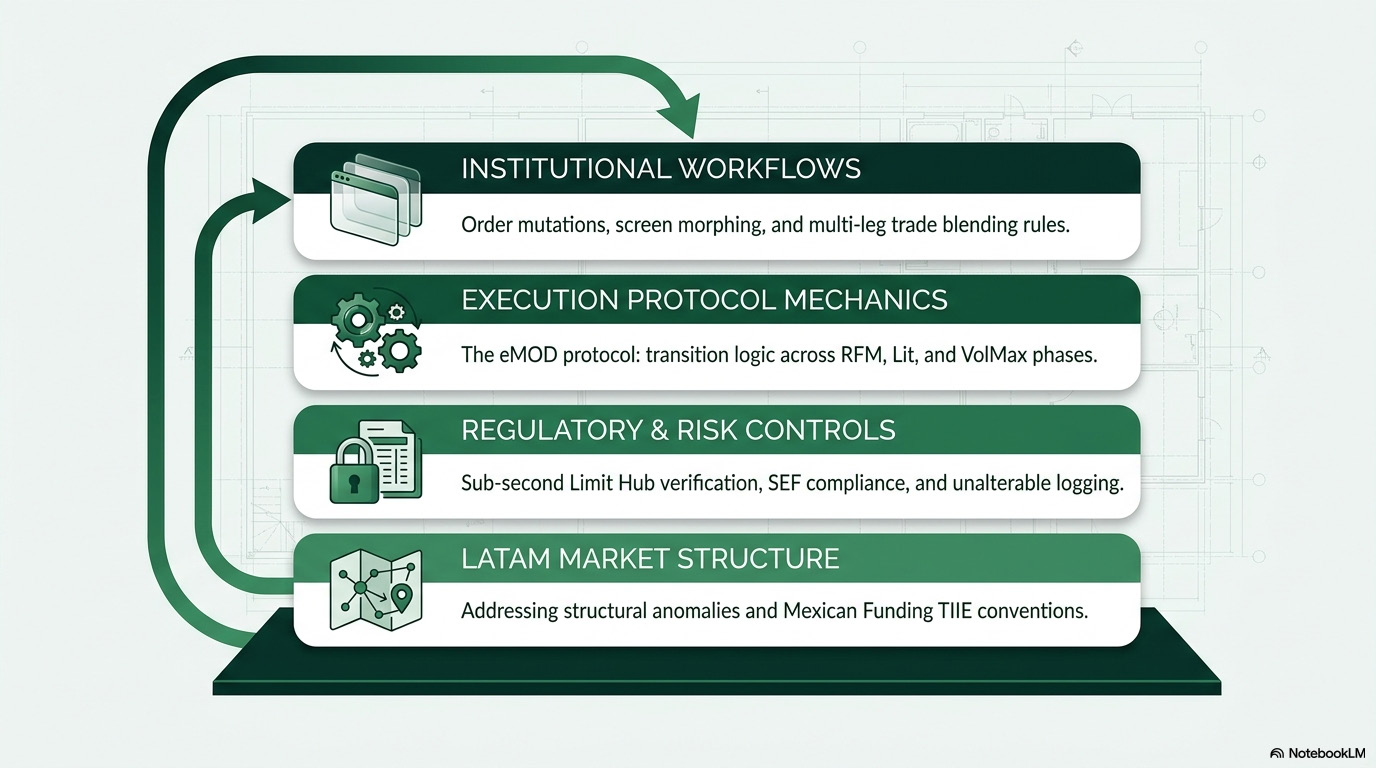

The platform’s convention model must support both standardized and more granular swap structures. Standard tenors allow recurring liquidity to form around familiar points on the curve, while custom tenors allow participants to express more specific hedging or risk-transfer needs. Internal product discussions refer to multiple tenors being open in the trade module and emphasize that tenor behavior is a formal part of the platform specification rather than an incidental UI detail.

IMM dates add another layer of convention control. OMeT discussions reference specific IMM structures such as “91IMM March” and “91M IMM June,” and describe IMM rolls as transactions that may extinguish risk in one IMM date while creating or adding risk in another. This matters because IMM-linked swap structures are not just alternative maturities; they create distinct risk buckets, roll behavior, and clearing/reporting considerations that must be handled consistently by the platform.

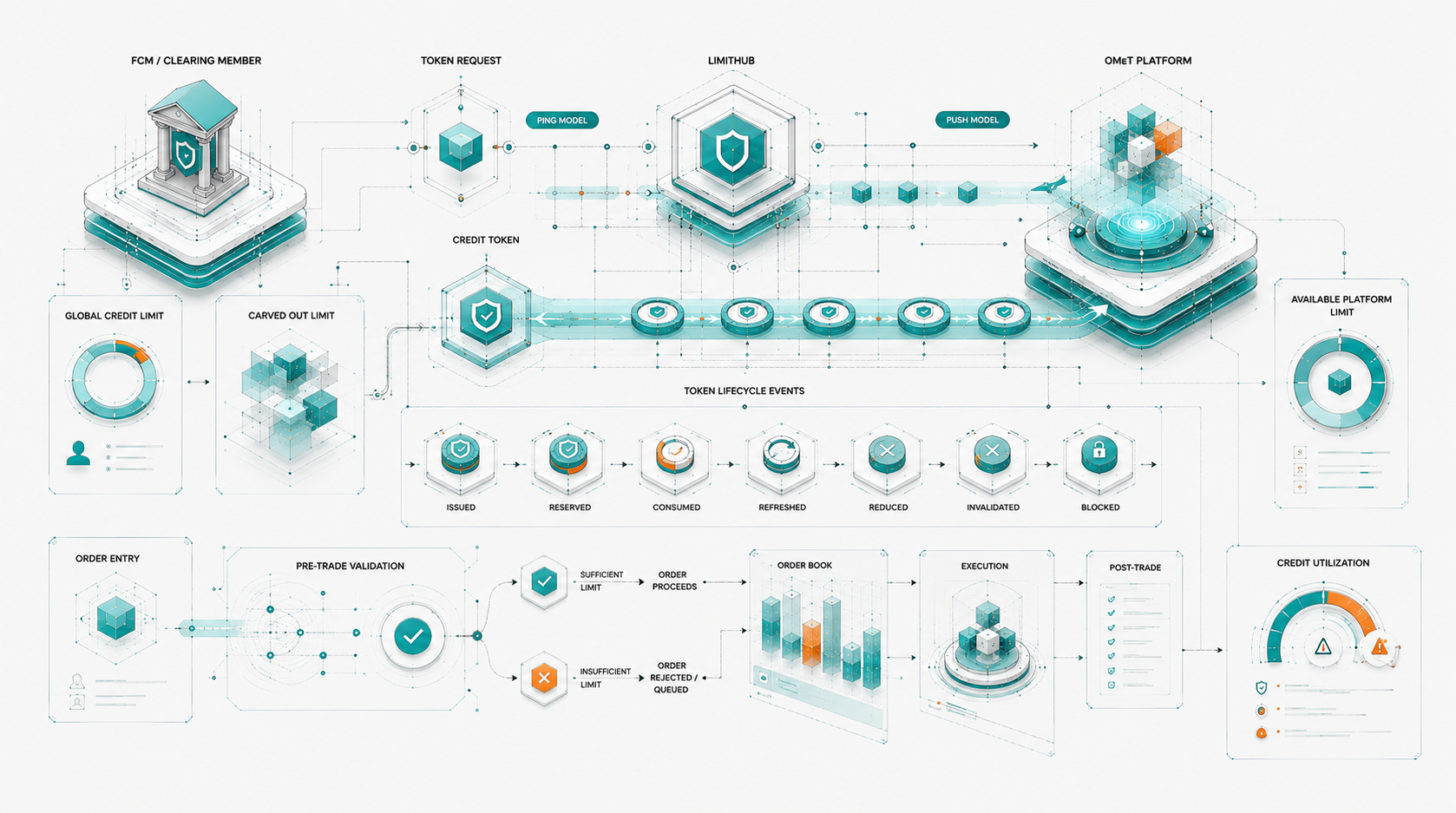

Operationally, these parameters feed directly into execution and risk controls. Tenors may be subject to different matching logic, spread controls, and credit validation behavior, and internal discussions note the decision point between leaving tenors on midpoint matching versus changing them to price-time matching to avoid unexpected outcomes in active sessions. For institutional users, the value is a convention layer that can support TIIE OIS structures, IMM dates, and custom tenors without forcing them back into manual negotiation or post-trade correction.