OMeT market data feeds begin with the live signals produced by the execution engine: bid, ask, last, and depth-of-book. Internal product discussions define market data in exactly those terms, while also noting that OMeT’s broader strategy treats market data as one subset of a larger institutional data layer. That distinction is important because a cleared swaps venue does not only generate prices; it also generates workflow telemetry around requests, quotes, amendments, matches, residual liquidity, and clearing progression.

Real-time depth-of-book telemetry gives participants a structured view of where liquidity is forming during active market phases. In OMP, the feed can expose visible bid and offer depth, last-trade context, order-book movement, and changing market pressure across supported instruments and tenors. This data is especially valuable in markets where legacy voice workflows leave participants dependent on fragmented indications rather than a consistent electronic view of executable interest.

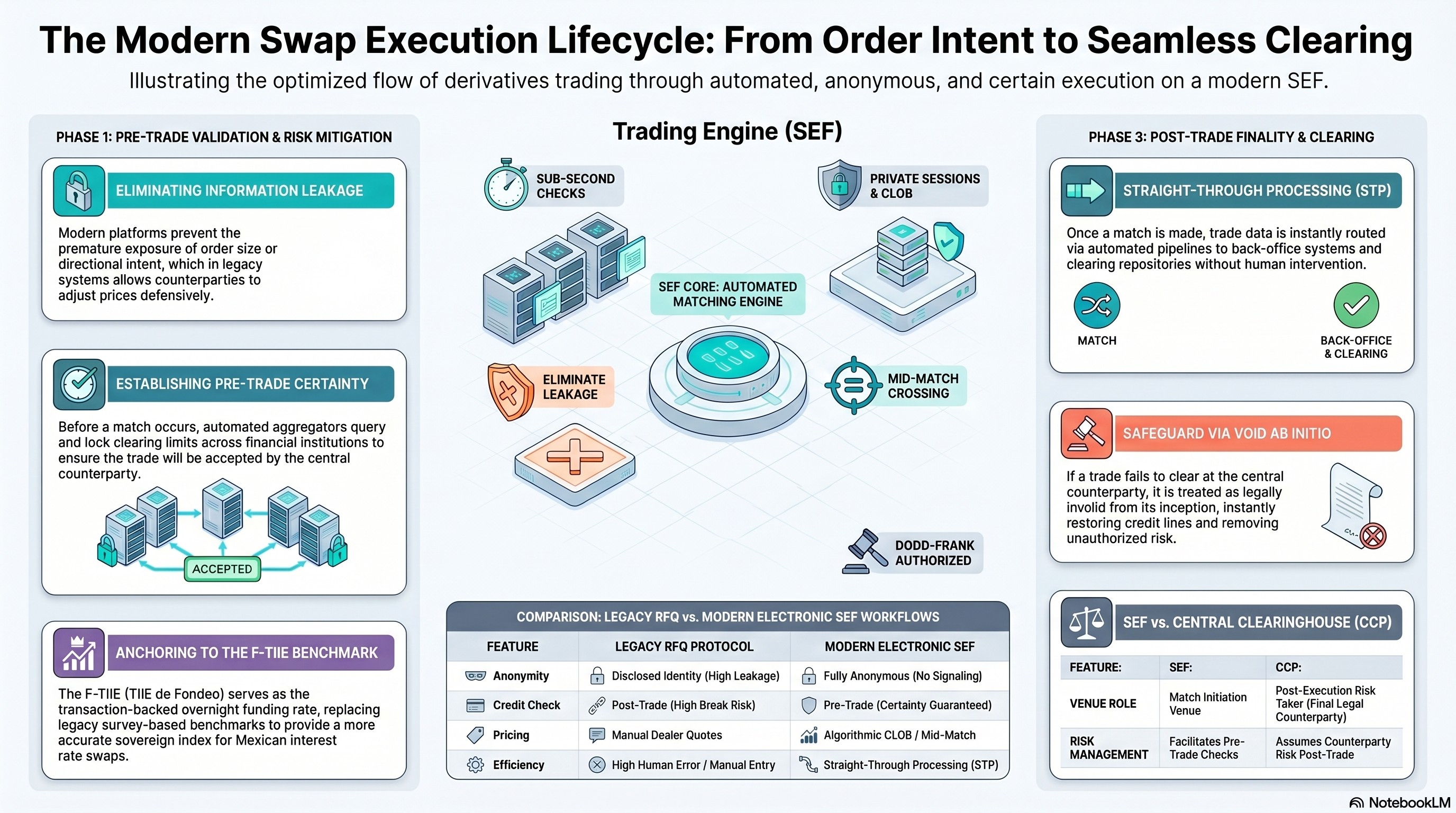

Historical pricing curves extend that visibility beyond the live session. OMeT’s LATAM strategy includes a dashboard featuring delayed F-TIIE fixings and basis swap curves as a recurring engagement layer for traders and risk managers. Over time, these historical curves can support execution benchmarking, liquidity diagnostics, relative-value review, and market-structure analysis across Mexican TIIE / F-TIIE products and future regional cleared derivatives.

The analytical integration path connects raw feed data to OMeT Intelligence. Real-time depth, historical curves, execution events, and workflow state changes can be routed into dashboards, APIs, Waterfall views, and custom query tools. OMeT materials describe the platform’s data strategy as moving beyond basic market data into broader analytics and reporting, including institutional sales intelligence and high-intent data products. The result is a market-data architecture that does more than display prices; it turns execution activity into a reusable analytical layer for trading, risk, compliance, and product strategy.