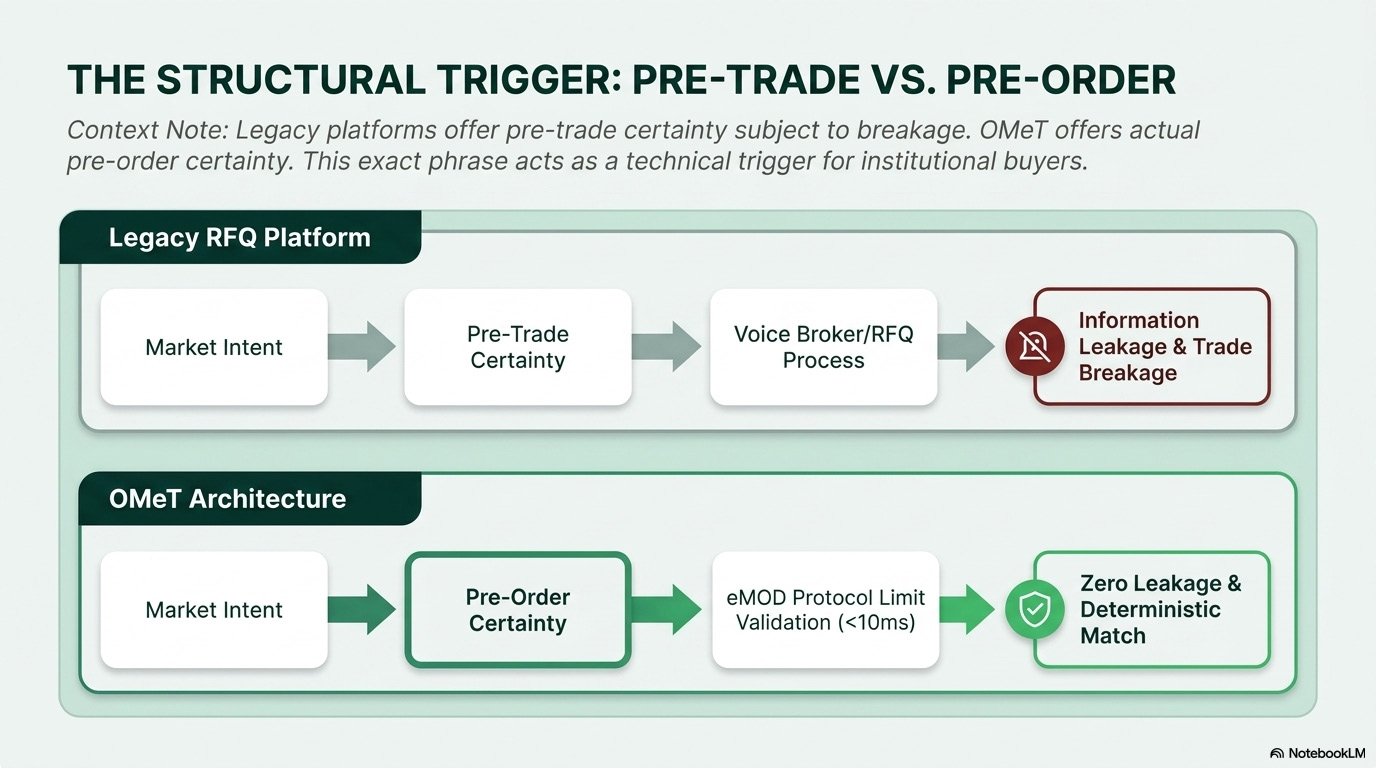

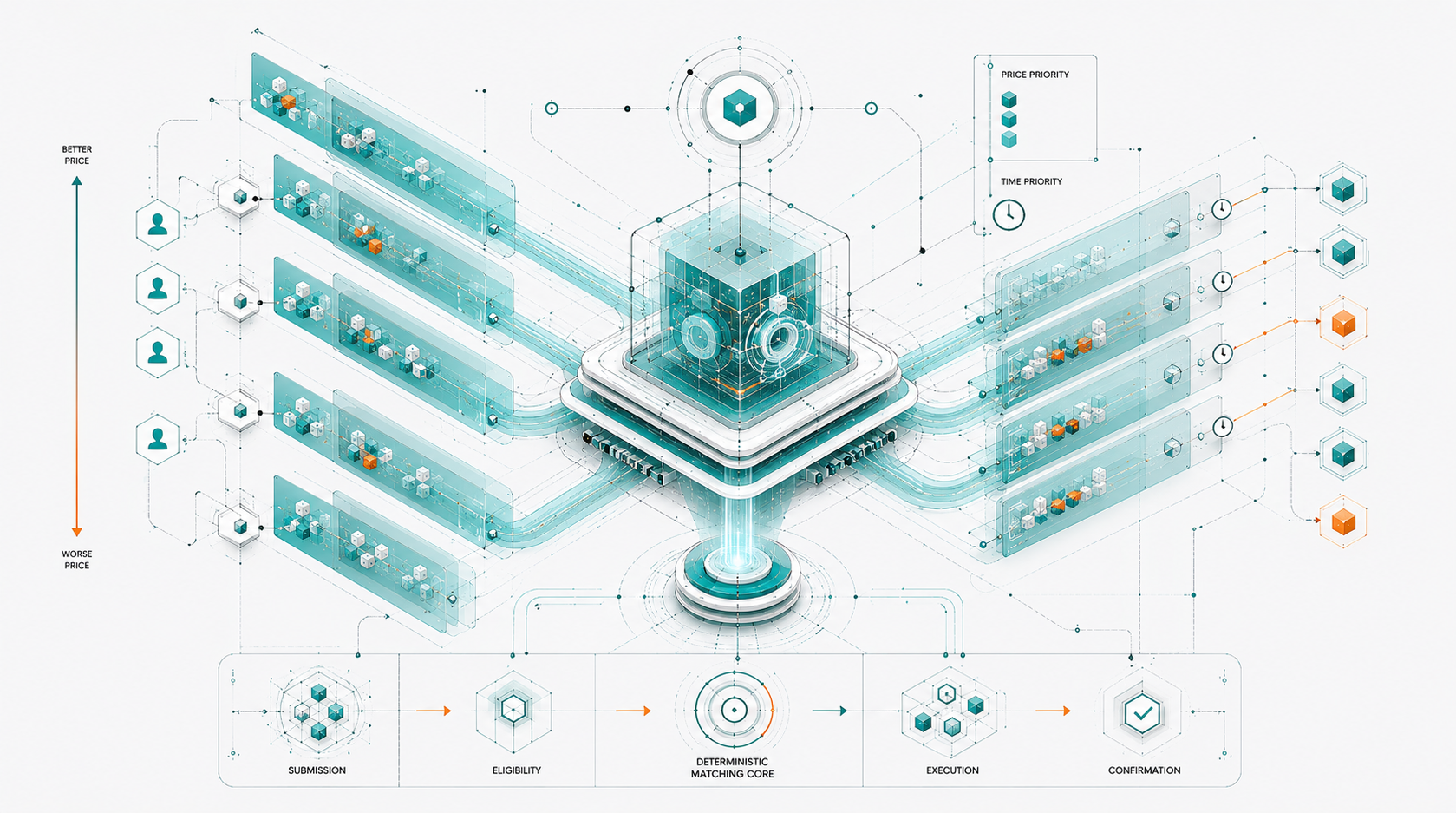

Information leakage is most acute when a large asset manager has to expose an outsized block directly to a fragmented market. In a traditional voice or RFQ workflow, the request for price can become a signal before execution begins: the market may infer the requester’s direction, urgency, and total position size. Once that information circulates, liquidity providers can widen markets, step back, or reprice against the trader before the full order is completed.

OMeT’s Sociable Size concept is designed to contain that exposure. Instead of forcing the buy-side desk to disclose the full underlying position at the point of price discovery, the protocol standardizes the visible request around a smaller, uniform baseline amount. Internal platform materials describe this as asking liquidity providers to make a two-way market on a predefined, smaller nominal amount, creating an “iceberg effect” that lets providers quote on a manageable size while reducing the perceived risk of engaging with a much larger trade.

This matters because the visible size becomes a market-control parameter rather than a confession of full intent. The requester can test executable pricing without telling the entire market how much risk ultimately needs to move. Internal testing discussions also reflect this principle: full size remains hidden while a nominal size is shown during the relevant phases. The protocol therefore separates price formation from full-size disclosure, reducing the chance that competitors or liquidity providers can reverse-engineer the trader’s complete position.

For large buy-side desks, the result is a safer path into liquidity discovery. Sociable Size gives market makers a standardized amount they can price confidently, while preserving the requester’s ability to manage larger residual risk through later controlled workflow stages. In OMeT’s broader architecture, this supports the same institutional objective as its execution stack: a deterministic environment for cleared OTC markets that connects execution, allocation, post-trade workflow, and market intelligence without relying on fragmented manual signaling.